Disclaimer: This is not investment advice

In September I wrote up my investment case for dLocal ($DLO), in which I expressed a positive view on the fundamentals of the business and on the company’s growth prospects. To recap, this was predicated on the idea that, in contrast to most merchant acquirers who have attractive business models (assuming they can reach sufficient scale) but see their economics eroded by a fragmented and competitive marketplace, dLocal might be able to create higher switching costs and barriers to entry for its business via its exclusive focus on partnering with global merchants across a variety of emerging market countries. I thought this could help them create customer lock-in and drive high net revenue retention for years to come. There was also the idea that dLocal was generating much higher net take rates versus competition as a result of FX conversion fees and higher authorization rates. I tempered my final conclusion with caution on valuation and decided to take a small position with the potential to average down if appropriate. I wrote that when the stock was trading at $24.30. As of yesterday’s close, DLO was trading at $21.22. I hadn’t actually done any averaging down since my report, mainly because I’ve been struggling to get the valuation to warrant a proper position given my outlook for interest rates.

Yesterday, however, Carson Block of the respected short-selling firm Muddy Waters announced at the Sohn Conference in London that the firm is short dLocal and that the company “is likely a fraud.” They have published a detailed 47 page report that lays out their analysis and substantiates their views / allegations. You can download the full report here. After this bombshell, the stock sold off 51%.

The timing of this is interesting, as dLocal had reported Q3 2022 results the day prior. Even though the company reported strong revenue growth and progress on a couple of key long-term metrics that I pay attention to, such as the number of countries per merchant and revenue growth in Asia & Africa, I became pretty nervous after reading through the call transcript. Management did not answer all of the questions posed by analysts in a candid way. In some cases they stuck to a party line about being “very proud of the quarter” etc etc. They seemed cagey and vague when responding to pretty obvious questions, such as details around new FX regulations in Argentina and payment method mix in new geographies. It struck me as bizarre. I thought that this probably reflected inexperience, as management teams can feel as though they need to put a positive spin on everything, but the way in which they spoke made me wonder whether their tone conveyed inexperience or evasiveness.

Taken together, the report by Muddy Waters and the tone of management comments on the recent call warrant a reappraisal of my investment case for dLocal, I believe. I will look at each in turn below.

Muddy Waters Report

I read the full report by Muddy Waters yesterday, so let me go through their key points and offer some thoughts on each.

Re-stating Total Payment Volume (TPV) materially (and not re-stating revenue)

MW points out that dLocal reports TPV over time for each of their annual cohorts from 2018 through 2021, but has restated some of these significantly. See below for 2019 and 2020. The first year’s TPV of the 2019 cohort was revised down from $471M to $56M (i.e. by 88% !) and the first year’s TPV of the 2020 cohort was revised down from $343M to $260M.

The first set of numbers were disclosed in the company’s F-1, while the second come from the Q4 2021 results presentation.

Exhibit A: F-1

versus Exhibit B: Q4 2021 Presentation

This really is weird, especially as such a glaring revision is hiding in plain sight (although I suppose that’s often the case with these things). I’m trying to think whether there is something we could be missing here, perhaps some frame of reference that is different between the two disclosures that is poorly noted in the presentation. Taken at face value, the implication is that revenue for 2019 and 2020 might have been overstated. I am not sure what to make of this. At best it seems weird, at worst it could be egregious.

Conflicting foreign currency receivables disclosures

MW points out that dLocal disclosed two different numbers for its foreign currency receivables in its F-1. This is important for MW’s case as they believe that dLocal is using FX to inflate revenues. See the discrepancy MW points out below:

MW the points out that dLocal settles on the higher of these two numbers ($49.8M) in their October 2021 secondary offering, but then reverts back to the lower number ($45.6M) in their 2021 20-F. They then stop disclosing in that document local currency trade and other receivables.

A charitable interpretation here could be that dLocal is in the business of managing 20+ different currencies and so, given such complexity, it is possible that this discrepancy reflects an honest mistake in reporting. But, you know, this is dLocal’s core business, so they really should be all over it. I’m not sure that this, in isolation, is evidence of nefarious purposes, but it does present what should be immutable data as mutable.

Conflicting payable vs receivable accounts between subsidiaries

MW points out that the vast majority of dLocal’s revenue is processed via three subsidiaries, one in Malta and two in the UK, but that there is a serious discrepancy in the 2020 reporting of these subsidiaries when they are compared against each other. Here is how MW summarizes their observation (emphasis mine):

DLO has three primary operating subsidiaries – DLocal Ltd (Malta) (“Malta Operating”), DLocal LLP (UK) (“UK LLP”) and DLocal Corp (UK) (“UK Corp”) – which in turn sit at the top of a network of local subsidiaries. In 2019 and 2020, these subsidiaries respectively accounted for ~94.9% and ~90.5% of consolidated revenue. UK LLP’s 2020 financials show that as of December 31, 2020, it owed Malta Operating $15.7 million. Malta Operating’s 2020 financials show that as of December 31, 2020, it is owed by all related parties a total of only $12.4 million. In other words, UK LLP’s financials show that it owed Malta Operating 26.6% more than Malta Operating’s financials show it could be owed.

We understand that substantially all of cross-border payments that DLO processes pass through these three subsidiaries. Two of these subsidiaries’ financials, which are available from the UK Companies House and the Malta Corporate Registry, are in opposition to one another in the flow of funds, bolstering our view that DLO’s accounts are materially misstated. The primary subsidiary DLocal LLP (UK) (“UK LLP”) shows an account payable owed to the primary subsidiary DLocal Ltd. (Malta) (“Malta Operating”) that is contradicted by Malta Operating’s filings.

Obviously something is wrong here, but MW doesn’t hypothesize about what exactly is wrong. This observation is presented less as a sign of deliberate malfeasance in isolation, but more as as part of a patchwork of things that don’t add up. MW believes, based on experience, that such a patchwork might suggest evidence of fraud.

Fraudulent accounting of timing and funding of large pre-IPO stock option exercise by founders

MW believes it has found “one instance in which it is almost certain that DLO fraudulently changed its accounts in order to disguise the facts of a particular set of transactions. In other words, DLO has seemingly shown that it has crossed the Rubicon of changing its accounts to try to conceal the facts, and then it told investors an untrue version of events. We suspect that DLO altered its accounts to avoid the negative optics of making a large loan to its senior management pre-IPO.”

Essentially, in November 2020 dLocal entered into an agreement with CEO Sebastian Kanovich and President Jacobo Singer to lend them $31.5M ($20.5M to Kanovich and $11M to Singer) at 1.5% annual interest in order to provide them with liquidity to exercise certain options pre-IPO. The company’s total cash on the Balance Sheet as of December 2020 was $112M, meaning the loan principal represented 28% of total cash - clearly a non-trivial sum.

MW points out that in the company’s F-1 from May 2021 the disclosure indicates that the loan was funded and the options were exercised:

But then in the 424B1 filing in October 2021, the disclosure changes and indicates that the loan was not funded as of December 2020 and the options were not exercised by that time. You can see from the below that the disclosure in the 424B1 filing is almost identical to the above, but the note about the outstanding loan balances has been removed:

If you check note 2.11.3 on the Employee Share Purchase Plan (ESPP), it defines the loans to Kanovich and Singer as being outstanding as of the point at which their options are exercised and says explicitly that as of December 31st 2020 the options had not been exercised and therefore the loans were not outstanding.

However, this contradicts the F-1 note on related party transactions from May 2021 which said that on December 31st 2020 the full $31.5M loan balance was outstanding, implying that Kanovich and Singer had exercised their options. In both reports the loans are cited as having been fully repaid by April 2021, but in the first report the inference is that Kanovich and Singer exercised their options in December 2020, while in the second report it is that they exercised some time in Q1 2021. What’s more, I also checked note 2.11.3 of the May 2021 F-1 and that section contains identical wording to section 2.11.3 of the 424B1 and contains the same sentence “As of December 31st, 2020, the loan repayment had not started and therefore neither the shares nor the loan, were outstanding.” So the F-1 is in contradiction not only with the 424B1, but also with itself.

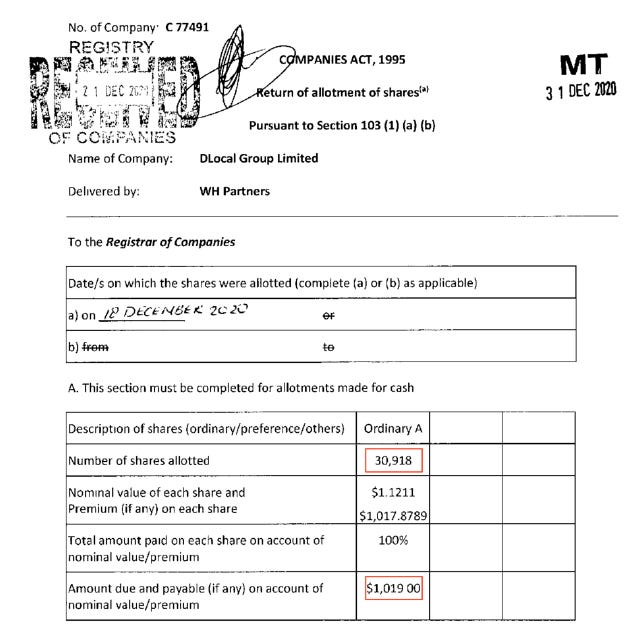

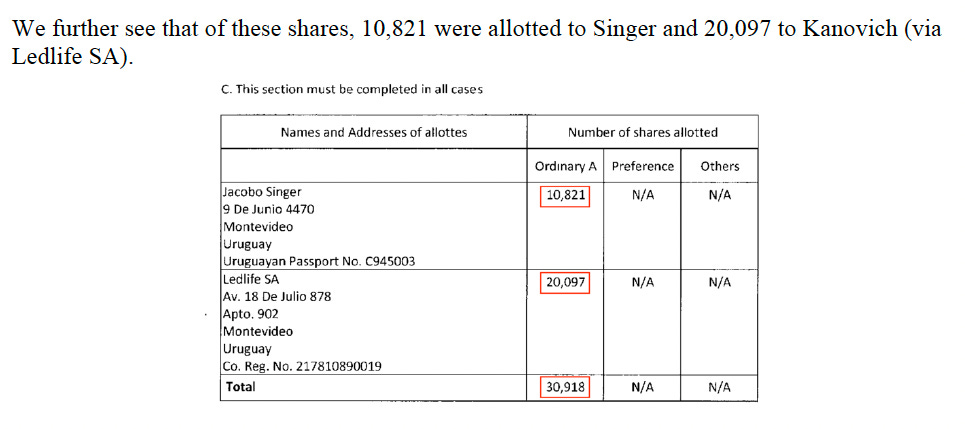

Perhaps you could view the original disclosure in the F-1 about the loans being outstanding as a mistake, but MW points out the the Malta subsidiary filings indicate clearly that the loans were indeed funded and shares allotted to Singer and Kanovich in December 2020. The Malta Company Registry shows that on December 18th, Malta Group allotted Kanovich and Singer a total of 30,918 shares at $1,109 per share, totaling $31.5 million. MW also provides evidence of wire transfers from dLocal to Kanovich (via Ledlife SA) and Singer on December 17th 2020, one day before their shares are allotted.

In other words, only one section from four sections among two separate SEC filings indicates that Kanovich and Singer exercised their options in December 2020, with the rest implying that this happened at a later date in Q1 2021. And yet the subsidiary filings indicate that the shares were exercised on December 18th.

MW theorizes that the company has fraudulently revised its accounting disclosures to cover up the poor optics of a large loan made to insiders pre-IPO, settling on a final account in which “i) DLO entered into the loan agreement in November 2020; but ii) the options were not exercised until March and April 2021; and iii) the exercises were funded with outside money – not with the loan. In other words, the exercises occurred in the following fiscal year and the loan was effectively never funded.” Personally, I’m not getting from these discrepancies that they’re trying to pretend the loan was never funded, but rather that the timing of the option exercises is either being misreported or obscured. Both SEC filings say the loan was fully repaid in April 2021.

MW further points out that share counts on March 1st 2021, after the share sale to General Atlantic, show Kanovich (Ledlife SA) and Singer were again allotted their full amount of shares. This corroborates the idea that they are trying to create the appearance that the options had not been exercised in December 2020, despite what the subsidiary filings show. Why? I have no idea. MW does some more theorizing, this time linked to potentially suspect use of funds surrounding dLocal’s acquisition of PrimeiroPay.

The purpose of re-allotting the shares in 2021 appears to have been to enable Singer and Kanovich to fund the exercises with $31.5 million of outside capital, rather than a loan from DLO. Each was 30 years old at the time of the IPO.7 We certainly have to tip our caps to two young go-getters who are able to access such liquidity at only 30 years of age. That said, given that they were going to borrow the money from DLO only four months earlier, they seemingly did not have access to such liquidity in December 2020.

We note that Kanovich had been CEO of AstroPay, and Singer “led product and engineering teams at AstroPay.” It’s possible they obtained such liquidity as a result of their time at AstroPay. It’s also possible they were able to obtain financing from third parties based on their stakes in DLO (and possibly other assets). There are of course other ways they could have obtained this liquidity in March and April of 2021.

Regardless, it does strike us as an interesting coincidence that Kanovich and Singer funded these payments at the same time DLO sent $38.7 million to purchase the assets of PrimeiroPay – and the $38.7 million was actually a prepayment. It further strikes us as curious that the Managing Director and major shareholder of PrimeiroPay subscribed to DLO shares at a private market valuation just under three months before the IPO for $1.4 million, and at around the same time as DLO made its prepayment. There’s an old legal adage that when it comes to property “possession is nine-tenths of the law.” Based on our experiences working in emerging markets, we believe that this advice is particularly on-point.

I don’t think I grasp fully what is going on here, but it does seem strange. The most charitable interpretation might be that dLocal’s reporting of the option exercise loan agreement was just a befuddled mess. But that’s also not a great interpretation.

Take rates might be artificially inflated

As I pointed out in my original piece on dLocal, they have take rates significantly higher than competitors - around 2.3% versus 0.2% for Adyen. My understanding was that this reflects the share of revenue of FX conversion fees (which could be up to half of revenue) and also the greater complexity of the transactions / the higher authorization rates dLocal can deliver for merchants compared to peers. Well MW believes this is too good to be true and that the company might be overstating their take rate materially. Taking the growth in net take rate in 2020, their skepticism boils down to the following:

DLO’s Take Rate spiked in 2020, growing 17.5%. Not only is the growth remarkable to us, but the fact that it didn’t compress in 2020 instead strikes us as highly suspect. The Take Rate seemingly should have fallen in 2020 because:

DLO’s lowest take rate cohorts, 2018 and 2020, increased their collective share of TPV from 43% in 2019 to 59% in 2020. Each cohort has a 2020 Take Rate significantly lower than DLO’s reported overall Take Rate. (As we discuss infra, the 2020 cohort has conflicting TPVs, which in turns implies it also has conflicting Take Rates due to the conflicting cohort TPV disclosures discussed supra.)

In 2020, DLO apparently began strongly ramping up its local-to-local business, which has a much lower margin. (As detailed infra, approximately half of DLO’s gross Take Rate comes from FX.) We understand that Google began using DLO in mid-2020, and it quickly became its largest customer by TPV. However, we also understand that Google negotiated very low fees, and that it principally uses DLO for local-to-local transactions.

Our research corroborates that of an investment bank analyst in that the sentiment in the industry is DLO at most charges a slight premium to its competitors, if not offers comparable pricing.

They subsequently produce corroboration for each of these points, including interviews with former dLocal executives, which I won’t go through here for the sake of brevity, but it struck me as reasonably persuasive on the whole. Bullet points two and three are very important, because they suggest that dLocal’s value proposition does not extend to pricing power, something the company claims it does in fact have as a result of the complexity it handles on behalf of merchants and the power of its one API / one contract model. Per the second bullet, the fact that merchants are establishing a local presence in emerging geographies and ramping local-to-local business is concerning, because it suggests that merchants are sensitive to the FX conversion fees they give away by having dLocal handle cross-border volumes. From dLocal’s perspective this threatens a big chunk of their take rate. So if I was thinking that the company’s prowess in emerging markets might translate into superior economics, their merchant clients are rather taking everything they can get and giving little in return.

MW believes the take rate is propped up mainly by FX fees and gains. They estimate FX fees and gains represent 40-50% of revenue. I guess this would be ok, if precarious, but MW believes this revenue share to be fictitiously high. MW estimates that Ebanx, a large local Brazilian competitor, generated FX gains and fees amounting to ~0.6% of cross-border TPV compared to ~3% on cross-border TPV for dLocal. Yet MW estimates that the true number for dLocal should have been ~1.5%. This number is partially informed by speaking to a former company executive, confidentially of course. They also cite corroboration via a 2021 investment bank research report cited a report by the Brazilian Central Bank as showing that FX spreads on non-export contracts typically are ~1.2%.

Concerns about client funds segregation

In my original report, I mentioned that it is important to remove most of trade receivable and trade payable from net working capital when calculating free cash flow, as these line items contain funds held on behalf of clients. MW has performed a reconciliation of dLocal’s Cash Flow Statement to the Balance Sheet for 2020 at the consolidated level and adjusting for client funds. They show that the reconciliation after stripping out client funds shows that dLocal ended 2020 with $3.3M more cash than the net change in cash on the Cash Flow Statement implies. They infer that this could mean that “either DLO’s disclosures are inadequate (i.e., more detail is needed to disaggregate merchant account balances from those of DLO), inaccurate, or DLO likely used client funds for its 2020 cash needs.”

The discrepancy is larger at the Malta subsidiary, showing a $4.1M delta. As MW points out, such a discrepancy is even less justifiable at the subsidiary level, which lacks the accounting complications related to consolidation. Again, in isolation this does not constitute evidence of malfeasance, but it is another data point that does not add up.

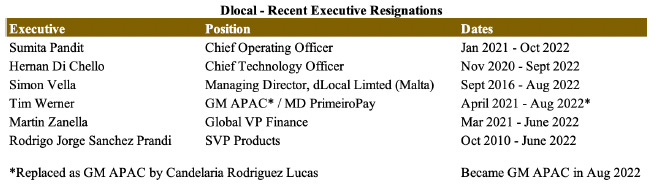

Insider departures

Since June 2022, there has been a wave of senior executive departures. See the table below:

MW likens this to “rats fleeing a sinking ship”……There could be good reasons for all of these, theoretically, but I do agree that this is a very concerning sign. Such a torrent of departures at a senior level rarely indicates good things. Again, at best it could indicate a poor culture and/or incompetence, at worst…something else.

The Muddy Waters report details several other points, which I won’t go through here in detail, but these include deficiencies in back office systems/controls, breaches of Malta Tier 1 Capital Requirements, a seeming desire to evade FCA regulation of the UK subsidiaries, a dodgy choice of UK auditor, and entanglements with former parent entity AstroPay.

All in all, the report raises some serious questions. I am not sure I follow how Muddy Waters arrives at all their conclusions, but they provide enough evidence and analysis to make me pretty concerned.

dLocal issued a statement about MW’s report toward the end of yesterday and it said the following:

The report contains numerous inaccurate statements, groundless claims and speculation. Short seller reports are often designed to drive the stock price downwards to serve the short seller’s interests to the detriment of the company’s shareholders. We caution shareholders from making investment decisions based on this report. dlocal will rebut the allegations in the appropriate forum in due course.

This offers very little signal.

Q3 2022 Earnings Call

In the earnings call for Q2 2022, dLocal’s management team, above all CEO Sebastian Kanovich, seemed oddly defensive when answering some innocuous questions. I didn’t read too much into it at the time. In the call transcript for Q3 2022, however, I noticed some of the same thing and it started to make me feel a little nervous, even before Muddy Waters dropped their hammer. I’ll go through a few responses to illustrate what I mean.

In their results materials, dLocal called out that Latam revenues were impacted by a change in FX regulations in Argentina, affecting cross-border volumes in the country. As a result, Latam revenue was actually down slightly quarter-on-quarter (up 7% QoQ excluding Argentina). Naturally people might want to know what had happened. But in response to the analyst from Morgan Stanley asking exactly this, Kanovich responded as follows:

Jorge, thanks for the question…So Jorge, we've been navigating a complex situation in Argentina from the beginning of this current quarter. If anything, what we've seen is that typically in Argentina, things get tougher at first and then as months or as weeks go by, there's more clarity around the local framework. If anything, we see everything trending on the right direction. Obviously, Argentina, it's a complex country. It represents as no other country of ours. It's not a big portion of what we do. But we also can know that deal with complex geographies. And part of the value that we bring to the table is continuing to navigate countries and situations like this. We've been in Argentina from 2016. We've been through ups and downs in all the creativity that the local government has had. And so far, we've been able to navigate it. If anything, we are very comfortable today because we've seen things trending in all the right directions also coming into Q4. How has it been for the Argentina growth? We probably could have added 4% to 5% more in revenues. But Jorge, I need to emphasize that we are extremely proud with the growth numbers we've shared today. Our Africa and APAC business is booming, and we think that's a key factor going forward. We continue to not have reliance on any particular geography. In situations like this, like the one we faced in Argentina will happen in emerging markets. It's expectable.

This answer provides zero useful information and tries to recenter the conversation on a party line about everything being great etc. It struck me as strange, because there is surely nothing wrong with just explaining exactly what happened in Argentina. Kanovich is right that in isolation it is not hugely material to the business, so in that case why not just explain what happened?

The same analyst repeated the question and Kanovich provided another answer that was only a modest improvement on the first:

Jorge Kuri: Thanks for that. I mean I appreciate that the company is resilient and that you adapt to changes. And I just -- sorry, I would really want to know exactly what happened. I'm not sure that the response was clear. What exactly happened? How did it limited your ability to grow your revenues? And what exactly is happening now that you feel that the situation has been normalized? If you can just be a bit more clear, so we can understand exactly.

Sebastian Kanovich: Sure. So typically, when the Argentina government comes up with new regulation around the FX, they come up with a very blanket regulatory framework where they say all of these industries are now restricted. In our experience working with the local central bank, they typically want to preserve the ability for global companies that are key to the population to access dollars. We are speaking about our merchant base who you know very well. So these are key services for the local population. So typically, what happens is while the initial regulatory change, it's very tough you see it flexibilizing over the weeks and months. There's also -- what Diego was mentioned. There's also some time, Jorge, it takes for banks to understand the new regulation and therefore navigated. So our expectation is that things will continue to evolve in Argentina. Obviously, it's a very volatile country. It doesn't represent much of our business. it's part of our business model to be able to navigate this stuff. And the reason why we are more confident because we are speaking from that. The last week of Q3 was 100x better than the first week of Q3, and therefore, we are seeing the trend and we're very comfortable going into Q4 and next year that things will continue to be doable for our merchants.

One other topic that came up was expansion into Asia and Africa. An analyst asked for colour on what has made the expansion successful:

Soomit Kumar Datta: A couple of quick questions, please. Again, firstly, just returning to Asia and Africa[….]was there anything in particular in this quarter, which was kind of happening countries coming online, a couple of merchants here or there? Is this the kind of run rate we should expect going forward just such a strong performance? And then secondly, on a related basis, please. I'm just curious what kind of card volumes or mix of card versus non-card are you seeing in these newer markets? I would assume that less card volumes and just wondered if that was having any impact on the economics of these transactions.

Sebastian Kanovich: Thanks very much for the question. So what has happened in both Africa and APAC is what we expected to happen, which is 1 API, 1 contract and us being able to bring our global merchants into the new region. 9 out of our top term merchants use us today in Africa and APAC. The opportunity ahead is massive. We've been bullish in this region, and we continue to believe that they're going to be a huge growth driver for us. We are not updating any guidance because that's not what we've done after practice. But we believe that there's plenty of opportunity ahead. [Jaco] can complement on that as [he] has been spending his time in South Africa, and […] can give you a much better view. And in terms of cards, the expectation -- what we've seen is very similar to what we've seen historically in other markets in LatAm. Some countries are card-heavy. Others are not that relevant. We -- as Jaco was mentioning before, we are payment method agnostic in the sense that we need to offer whatever payment method users want to pay with and we intend to continue to do so.

Another reasonable question, this time about something going well, and yet Kanovich in his response reverts to type about how great the business is rather than providing any colour that might be informative or useful regarding Africa and how it differs from Latam. He even mentions not updating guidance, which is not at all what the analyst was asking for. His response about payment method mix is vague, which might be fine in light of their stated indifference toward payment methods merchants want to accept, but it strikes me as too dismissive of what could be helpful information to aid analysts build an understanding of the idiosyncrasies of these markets. It doesn’t add up in a way, as part of how they frame their value proposition is in taking emerging markets that are different and complex and making them simple for merchants. And yet Kanovich appears to saying it’s all much of a muchness actually.

These responses do not present evidence enough by themselves to think something is amiss, but they did strike me as odd. Most good CEOs I have encountered are able to speak openly about their business, highlighting the good but not window-dressing the bad, in the process inspiring confidence in their ability to drive execution. Kanovich’s responses struck me as defensive when they did not need to be. I thought on the day of the results that the foolishness of this is that it would make people wonder about evasiveness when such worries were uncalled for. But the Muddy Waters report casts worries about evasiveness in a new light.

Conclusion

I am not sure whether dLocal is a fraud. In their report, Muddy Waters points out several discrepancies and raises some some serious concerns, but whether these constitute a fraud remains to be seen. They have been right before on that and could be right here too. In general, I have nothing against short sellers and believe they provide a valuable service to financial markets. Every walk of life needs someone willing to call out BS. That said, it is worth remembering that short-sellers are incentivized to draw the worst conclusions in public and there is usually enough grey area in the companies they analyze for them to defend the legitimacy of doing so.

But in a way this is already a moot point. They have pointed out enough discrepancies for one to draw two possible conclusions: 1) deficient controls and poor disclosures, 2) a deliberate attempt to cover something up. The second of these is much worse, but neither is good for an investor trying to find high quality stewards of capital. In addition, the point about lack of pricing power when dealing with large merchants like Google pokes a big hole in my prior notion that dLocal might be able to insulate itself better from competitive pressures.

When I take this alongside with the weird posture displayed by management on the most recent calls, I have enough to shake my confidence in the investment case pretty badly. I do not rule out the possibility that dLocal produces a robust rebuttal of all of MW’s allegations and reassures the market. But I’m not sure how prudent it would be to stick around to find out. I will exit my remaining small(er) position.